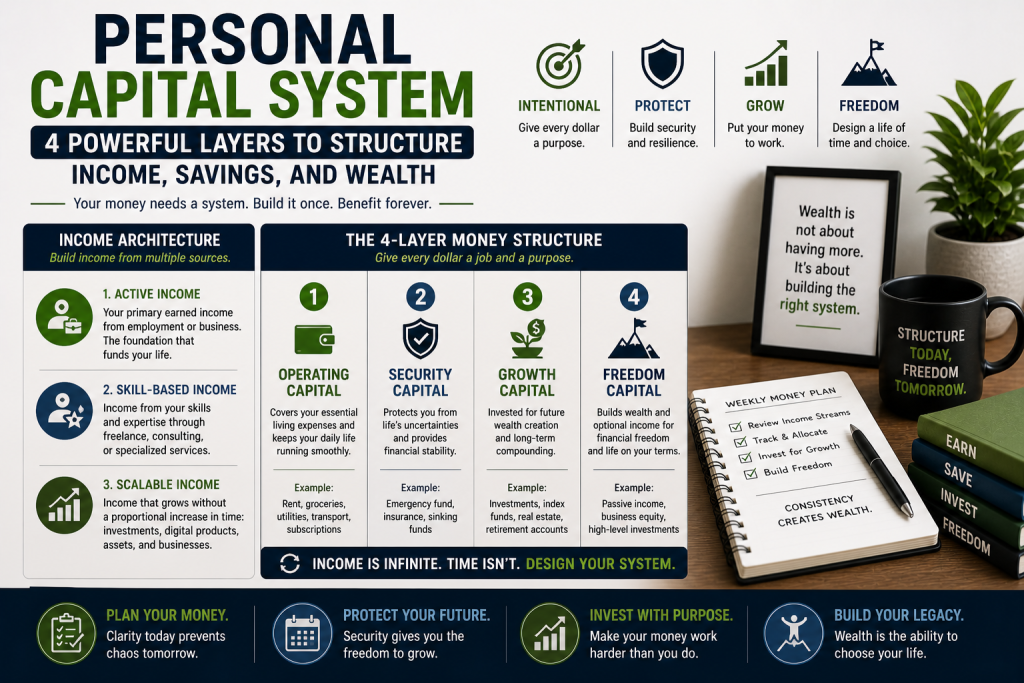

Personal Capital System: 4 Powerful Layers to Structure Income, Savings, and Wealth

A personal capital system is the difference between earning a solid income and actually building wealth — and most people are missing…

A personal capital system is the difference between earning a solid income and actually building wealth — and most people are missing it entirely.

If you have ever reached the end of the month wondering where all the money went, you already know the feeling. The problem is almost never how much you earn. It is the absence of a deliberate structure for how money moves, grows, and protects you over time. Without a personal capital system in place, income flows randomly through daily spending, scattered obligations, and impulse decisions — leaving little to show for the effort, regardless of the paycheck.

At Vida Lit, financial structure is a core component of the Life Operating System. A personal capital system is not about budgeting more aggressively or cutting out small pleasures. It is about designing a clear, intentional architecture for your money so that every dollar has a role — and your finances shift from reactive survival to deliberate, compounding control.

Here is the complete framework.

Why Most People Never Build a Personal Capital System

The most common financial trap is not overspending — it is operating without structure. And the consequences are more damaging than most people realize until years have passed.

Lifestyle inflation is the first silent killer. As income rises, spending rises to match it almost automatically, leaving savings and asset-building perpetually on the back burner. What feels like financial progress on the surface — a bigger apartment, a newer car, upgraded subscriptions — often produces zero real wealth growth underneath.

Lack of financial visibility compounds the problem. When there is no clear tracking or categorization, money disappears into the background noise of daily life. Decisions get made based on how the bank account looks at a glance rather than on any coherent long-term plan.

Short-term thinking locks the cycle in place. When finances are focused exclusively on the present — covering bills, managing immediate expenses, handling the next emergency — there is no room to plan for growth, freedom, or future security. Research on financial stress and decision-making shows that financial pressure narrows cognitive focus toward immediate problems, making long-term planning feel inaccessible even when it is most needed.

The result is a cycle where people feel perpetually stuck regardless of how hard they work or how much they earn. A personal capital system breaks that cycle by replacing reactive financial behavior with intentional structure.

What Is a Personal Capital System?

A personal capital system is a deliberately designed framework that organizes how money is earned, saved, protected, and grown — across multiple income sources and capital layers — so that your finances compound toward long-term security and freedom rather than cycling endlessly through short-term management.

The key distinction between a personal capital system and a simple budget is intentionality and architecture. A budget tells you what you spent. A personal capital system tells your money where to go before it arrives — and ensures that every layer of your financial life has a clear purpose.

Within the Vida Lit Life Operating System, a personal capital system has two structural dimensions: the Income Architecture that determines how money enters your life, and the Four-Layer Money Structure that determines what happens to it once it does.

The Income Architecture of a Personal Capital System

The first structural element of a personal capital system is how income is organized and diversified. Relying on a single income source — however reliable it feels — creates a fragile financial foundation. A well-structured personal capital system builds income across three distinct categories:

Active Income

Your primary earned income from employment, salary, or direct work. This is the foundation — the income stream that covers immediate operating costs and funds the other layers of the system. The goal here is not just to maximize this number but to ensure it is efficiently directed into the broader personal capital system rather than absorbed entirely by lifestyle spending.

Skill-Based Income

Income generated from specialized expertise applied flexibly — freelancing, consulting, coaching, or specialized services. This layer adds resilience and increases earning capacity without requiring a complete career change. Research on income diversification consistently shows that individuals with multiple income streams are significantly more financially stable and less vulnerable to economic disruption than those dependent on a single source.

Scalable Income

Income from ventures, digital products, investments, or assets that can grow without a proportional increase in time or effort. This is the long-term layer of the personal capital system — the one that eventually allows money to work independently of your direct labor. Building this layer takes time, but without it, financial freedom remains permanently theoretical.

Organizing income across all three categories transforms the foundation of your personal capital system from fragile to resilient.

The 4-Layer Money Structure of a Personal Capital System

Once income is structured, the second dimension of a personal capital system is how that income is organized and deployed. Dividing money into four distinct layers — each with a specific purpose — eliminates the confusion and emotional decision-making that defines most people’s financial lives.

Layer 1: Operating Capital — Your Day-to-Day Financial Engine

Operating capital covers the essential costs of your current life: rent or mortgage, utilities, groceries, transportation, and recurring necessities. The goal inside a personal capital system is not to minimize this layer at the expense of quality of life — it is to make it efficient and intentional so it does not silently expand to consume all available income.

A practical rule: operating capital should be the first layer defined, with a clear monthly number, so that every other layer of the personal capital system is funded from what remains — not from what is left over after unstructured spending.

Layer 2: Stability Capital — Your Financial Safety Net

Stability capital is your protection against disruption. It includes emergency savings, short-term buffers, and liquid reserves that cover unexpected events — job loss, medical expenses, urgent repairs — without requiring debt or financial scramble.

Financial research consistently shows that households with even a modest financial buffer experience significantly lower financial stress and make measurably better long-term financial decisions than those operating without one. Stability capital is not a luxury inside a personal capital system — it is the foundation that makes everything else possible.

A minimum target: three to six months of essential operating costs held in a liquid, accessible account — not invested, not tied up, available when needed.

Layer 3: Growth Capital — Where Wealth Is Actually Built

Growth capital is the wealth-building layer of your personal capital system. It is the money allocated to investments, assets, and opportunities that appreciate over time — stocks, index funds, real estate, business ownership, or any asset class aligned with your financial goals and risk tolerance.

This is where the compounding effect of a personal capital system becomes most visible. Money directed consistently into growth capital — even in modest amounts — compounds over years and decades into the kind of financial position that changes the trajectory of a life. The critical variable is not the amount. It is the consistency and the time horizon.

Note: This post discusses general financial concepts and frameworks. For personalized investment advice, consult a qualified financial advisor.

Layer 4: Opportunity Capital — Your Financial Flexibility Fund

Opportunity capital is what gives your personal capital system genuine agility. It is a more fluid, responsive reserve — separate from both stability and growth capital — that is available to deploy toward new ventures, strategic investments, skill development, or calculated risks when the right opportunity presents itself.

Without this layer, even well-structured finances can become rigid. Opportunity capital is what allows you to act deliberately when timing matters, rather than watching opportunities pass because your capital is either locked up or already allocated to immediate needs.

Financial Leverage and Optionality — The Long-Term Payoff of a Personal Capital System

When a personal capital system is functioning across all four layers, two powerful advantages emerge: leverage and optionality.

Leverage — inside a personal capital system — is not simply about borrowing. It is about using structured capital to generate more value than effort alone can produce. Investments that yield returns, skills that increase earning capacity, businesses with compounding revenue — these are all forms of leverage that a well-designed personal capital system is built to enable over time.

Optionality is perhaps the more underrated benefit. When your personal capital system is organized and each layer is funded, financial decisions stop being driven by pressure and start being driven by strategy. You can consider a career change, pursue a new opportunity, or take a calculated risk without the entire financial foundation being at stake. That freedom — the ability to choose rather than react — is the ultimate output of a functioning personal capital system.

How to Start Building Your Personal Capital System This Week

You do not need to overhaul your entire financial life at once. A personal capital system is built in layers, starting with the most foundational:

- Define your operating capital number — what does your current life actually cost per month? Get a specific number.

- Open a dedicated stability capital account — separate from your checking account, with a target of building to three months of operating costs.

- Identify one skill-based income opportunity — something you could offer as a service or freelance work within your existing expertise.

- Automate a fixed amount into growth capital monthly — even a small consistent amount begins the compounding process immediately.

- Run a weekly money review — 20 minutes, once a week, to track where money moved and ensure each layer is being funded intentionally.

This is not a complete personal capital system built overnight. It is the foundation — and foundations compound.

Frequently Asked Questions About Personal Capital Systems

What is a personal capital system? A personal capital system is a structured financial framework that organizes how money is earned, saved, protected, and grown across multiple income sources and capital layers. Unlike a budget, which tracks spending after the fact, a personal capital system designs where money goes before it arrives — so every dollar has a deliberate role.

How is a personal capital system different from budgeting? Budgeting focuses on tracking and limiting spending within existing income. A personal capital system is broader — it structures income architecture, organizes capital across four distinct layers, and builds toward financial leverage and optionality over time. Budgeting is one tool within a personal capital system, not the system itself.

How much money do I need to start a personal capital system? You can begin building a personal capital system at any income level. The framework scales — what changes with higher income is the amount flowing through each layer, not the structure itself. Starting with even a modest stability capital fund and a small automated growth capital contribution puts the system in motion.

How does a personal capital system connect to the Life Operating System? Within the Vida Lit framework, a personal capital system is one of the five control variables of the Life Operating System. Financial structure reduces chronic stress, expands decision-making freedom, and creates the stability that makes sustained focus and long-term growth possible across every other area of life.

Your Personal Capital System Starts With One Decision

Financial stability is not an income problem. It is a structural problem — and a personal capital system is the solution.

When income is diversified, money is organized across clear layers, and capital is deliberately directed toward stability, growth, and opportunity, finances stop being a source of stress and start being a tool for building the life you are actually trying to create.

This is what the Vida Lit Life Operating System is built around: not just productivity and focus, but the complete architecture of a life that compounds in the right direction.